APY Chart Explained: Complete Atal Pension Yojana Contribution Guide for 2026

14 May 2026 6 mins Personal Finance

India’s retirement landscape is changing rapidly. Rising inflation, increasing life expectancy, and uncertain income sources after retirement have made pension planning more important than ever.

For millions of Indians—especially those working in the unorganized sector—Atal Pension Yojana (APY) has become one of the most accessible long-term retirement schemes.

But one question confuses most people before investing:

“How does the APY chart work?”

If you’ve searched for:

APY chart

Atal Pension Yojana chart

APY contribution chart

APY calculator

APY monthly contribution table

…this guide will explain everything in simple language.

By the end of this article, you’ll understand:

What the APY chart means

How much you need to invest

Age-wise APY contribution details

Pension benefits after 60

APY vs other retirement schemes

Whether APY is worth it in 2026

What is Atal Pension Yojana (APY)?

Atal Pension Yojana is a government-backed pension scheme launched in 2015 to provide guaranteed monthly pension income after the age of 60. It mainly targets workers in the unorganized sector, including:

Small shopkeepers

Delivery workers

Drivers

Farmers

Daily wage earners

Freelancers

Self-employed individuals

The scheme offers a guaranteed monthly pension ranging from:

₹1,000

₹2,000

₹3,000

₹4,000

₹5,000

after retirement at age 60.

What is an APY Chart?

An APY chart is a contribution table that shows:

Your joining age

Desired pension amount

Monthly contribution required

Total years of contribution

The earlier you join, the lower your monthly contribution.

This is because APY works on the principle of long-term compounding and disciplined investing.

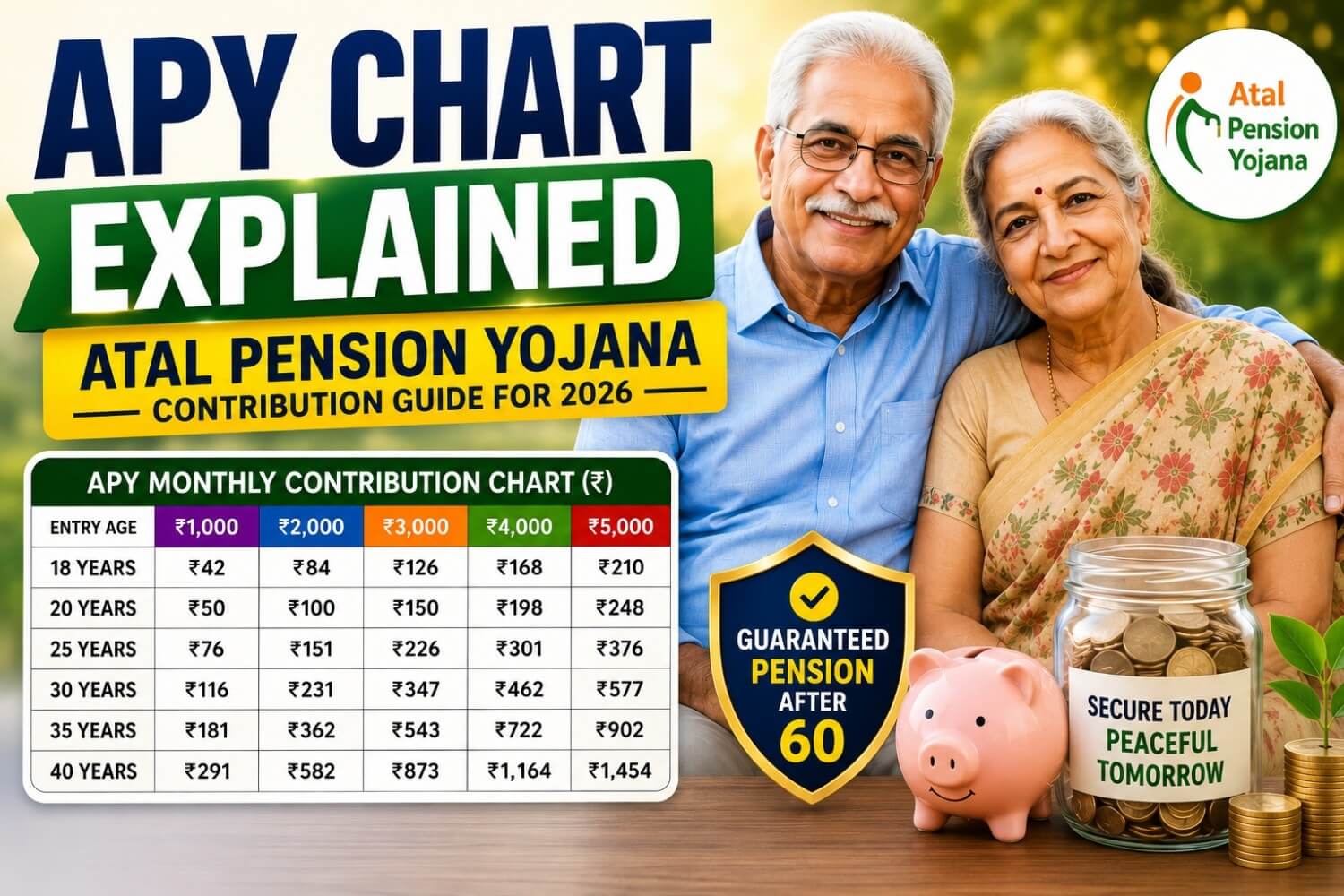

APY Chart (Monthly Contribution Table 2026)

Below is the most searched APY contribution chart for guaranteed monthly pensions.

APY ₹1,000 Pension Chart

Entry Age | Monthly Contribution |

|---|---|

18 | ₹42 |

20 | ₹50 |

25 | ₹76 |

30 | ₹116 |

35 | ₹181 |

40 | ₹291 |

APY ₹2,000 Pension Chart

Entry Age | Monthly Contribution |

|---|---|

18 | ₹84 |

20 | ₹100 |

25 | ₹151 |

30 | ₹231 |

35 | ₹362 |

40 | ₹582 |

APY ₹3,000 Pension Chart

Entry Age | Monthly Contribution |

|---|---|

18 | ₹126 |

20 | ₹150 |

25 | ₹226 |

30 | ₹347 |

35 | ₹543 |

40 | ₹873 |

APY ₹4,000 Pension Chart

Entry Age | Monthly Contribution |

|---|---|

18 | ₹168 |

20 | ₹198 |

25 | ₹301 |

30 | ₹462 |

35 | ₹722 |

40 | ₹1,164 |

For Detailed Calculations try APY Calculator - https://www.credyfi.com/calculator/apy-calculator

For Detailed Calculations try APY Calculator - https://www.credyfi.com/calculator/apy-calculator

The contribution amount increases with age because fewer years remain until retirement.

Why the APY Chart Matters

Most people ignore retirement planning in their 20s and 30s.

But the APY chart clearly shows one important reality:

Starting early dramatically reduces your investment burden.

For example:

A person joining at age 18 for a ₹5,000 pension contributes around ₹210/month.

A person joining at age 40 contributes around ₹1,454/month for the same pension.

That’s nearly 7x higher.

This is the power of long-term investing.

How APY Actually Works

Here’s the complete flow:

Step 1: Choose Pension Amount

You select your target monthly pension:

₹1,000

₹2,000

₹3,000

₹4,000

₹5,000

Step 2: Start Monthly Contributions

The amount is auto-debited from your bank account every month.

Step 3: Continue Till Age 60

You contribute regularly until retirement.

Step 4: Receive Guaranteed Pension

After 60, you start receiving monthly pension income.

The pension is backed by the Government of India.

APY Eligibility Criteria

You can join APY if:

Age is between 18 and 40 years

You have a savings bank account

You are an Indian citizen

The scheme is especially useful for people without EPF or corporate pension benefits.

APY Calculator: How to Estimate Contributions

An APY calculator helps you instantly estimate:

Monthly contribution

Total investment

Contribution years

Pension amount after retirement

Most APY calculators require only:

Your age

Desired pension amount

Based on this, the calculator estimates your required contribution.

Example of APY Calculation

Suppose:

Age = 25 years

Desired pension = ₹5,000/month

According to the APY chart:

Monthly contribution ≈ ₹376

Contribution period = 35 years

Total approximate contribution:

₹376 × 12 × 35

≈ ₹1.57 lakh

In return, you receive:

₹5,000 guaranteed monthly pension after 60

Is APY Really Worth It in 2026?

This depends on your financial goals.

APY is useful if:

You want guaranteed pension income

You prefer low-risk investments

You don’t actively invest in stocks

You work in the unorganized sector

You struggle with disciplined saving

APY may NOT be enough if:

You want inflation-beating retirement wealth

You seek high returns

You already invest heavily in mutual funds or NPS

The biggest limitation is that the maximum pension is capped at ₹5,000/month, which may not fully cover future inflation-adjusted expenses.

Still, APY can work well as a base retirement safety layer.

APY vs NPS: Which is Better?

Feature | APY | NPS |

|---|---|---|

Returns | Guaranteed pension | Market-linked |

Risk | Very low | Moderate |

Maximum pension | ₹5,000/month | No fixed limit |

Government backing | Yes | Yes |

Ideal for | Low-income earners | Long-term investors |

Flexibility | Limited | High |

A lot of investors today use:

APY for guaranteed income

NPS + Mutual Funds for wealth creation

This creates a balanced retirement strategy.

Benefits of Atal Pension Yojana

1. Guaranteed Pension

One of APY’s biggest advantages is predictable retirement income.

2. Government-Backed Security

The scheme is backed by the Government of India, making it relatively safe.

3. Affordable Contributions

Even low-income individuals can start with small monthly amounts.

4. Automatic Bank Debit

No need to manually pay every month.

5. Pension for Spouse

After the subscriber’s death, the spouse can continue receiving pension benefits in many cases.

APY Drawbacks You Should Know

A balanced financial decision requires understanding both pros and cons.

Limited Pension Amount

₹5,000/month may feel insufficient after 20–30 years because inflation reduces purchasing power.

Long Lock-In

You generally contribute until age 60.

Lower Wealth Creation Potential

Compared to equities or mutual funds, APY focuses more on safety than aggressive growth.

APY Subscriber Growth in India

APY adoption has grown massively in recent years.

In 2026, the scheme crossed 9 crore subscribers, showing increasing awareness about retirement planning among Indians.

This growth also reflects a larger shift:

People are realizing that relying only on children or family support after retirement may not be enough anymore.

Best Age to Join APY

The ideal age is:

18 to 25 years

Because:

Contribution remains very low

Long compounding period works in your favor

Financial burden stays manageable

The APY chart clearly rewards early investors.

Common APY Mistakes to Avoid

Ignoring Inflation

Don’t assume ₹5,000/month alone will be enough after 30 years.

Starting Late

Delaying entry sharply increases contributions.

Missing Contributions

Insufficient bank balance can lead to penalties.

Who Should Definitely Consider APY?

APY is especially suitable for:

Gig workers

Small business owners

Drivers

Rural workers

Self-employed individuals

Workers without PF benefits

People wanting guaranteed pension income

Final Verdict: Should You Use the APY Chart for Retirement Planning?

Yes—especially if you want a simple, low-risk, government-backed retirement plan.

The APY chart helps you understand exactly:

How much to invest

How early to start

What pension you can expect

While APY alone may not create complete retirement freedom, it can become an excellent foundational pension layer for millions of Indians.

The smartest strategy in 2026 is often:

APY for guaranteed income

Mutual funds/NPS for growth

Emergency savings for stability

Retirement planning works best when started early—and the APY contribution chart proves that clearly.

Frequently Asked Questions (FAQs)

What is the maximum pension under APY?

The maximum guaranteed pension is ₹5,000 per month.

Can salaried employees join APY?

Yes, eligible individuals with bank accounts can join.

Is APY tax-free?

Certain tax benefits may apply under existing tax provisions.

Can I increase my pension amount later?

Yes, APY allows pension slab upgrades in many cases.

Is APY safe?

Yes, it is a government-backed pension scheme.

What happens if the subscriber dies?

The spouse can continue benefits according to scheme rules.

Find the Best Mutual Funds for your every investment goal. Explore top mutual funds and start your SIP Today!

Find the Best Credit Card for your spending habits. Explore top credit cards and maximize your rewards.

Get a Personal Loan that fits your needs. Apply for loans from Rs 1000 to Rs 15 Lakhs with competitive rates.

Author - Abhishek Sonawane

Abhishek Sonawane, an MBA graduate from the prestigious Indian Institute of Management Visakhapatnam (IIMV), brings over ten years of experience in the finance domain. His extensive background includes various roles in financial management and strategy, providing him with a comprehensive understanding of the financial landscape. Abhishek’s expertise and dedication to financial education make him an authoritative voice in personal finance, helping readers make informed financial decisions.